When deciding between a personal loan and a home equity loan, it is important to understand the pros and cons of both types. Personal loans usually have higher interest rates and higher monthly repayments, while home equity loans are lower in monthly payments and have lower interest rates. A home equity loans can be an excellent option to help you make improvements in your home and get rid of credit card debt.

Lower monthly payments are possible with home equity loans

Home equity loans tend to have lower monthly payments that personal loans. Before you can benefit from this advantage, however, you need to meet certain requirements. First, you will need at least 15% equity. In addition, you need to have sufficient income. Your debt-to–income ratio (DTI) should be low. A DTI lower than 43% is preferred by most lenders. Your credit score should be excellent. A higher credit score will translate into better interest rates.

A home equity mortgage can allow you to borrow as much as 80% of your home's equity. Home equity loans are available to those with good credit ratings and minimal debt. You could get as much as $100,000. This loan cannot be repaid in full. The process takes longer. Home equity loans are more expensive than personal loans. You will need to wait longer before you can get funds.

Personal loans have higher interest rate

There are many things that differ between a loan for personal use and a loan for home equity. Personal loans are not secured, so the lender can't take your property if the loan isn't paid off. Home equity loans, however, require that you have sufficient equity in the home. A home equity loan may not be suitable for people who have bad credit or do not have enough equity in their home. Personal loans may be an option in this situation.

Home equity loans have lower interest rates, but personal loans tend to carry higher rates of interest than home loans. Because personal loans are more risky for lenders, they tend to carry higher interest rates. A personal loan's average interest rate is 8.83% for borrowers who have a 760 credit rating. Personal loan interest rates also include origination fees. These fees can range from 1% up to 8% of loan amount.

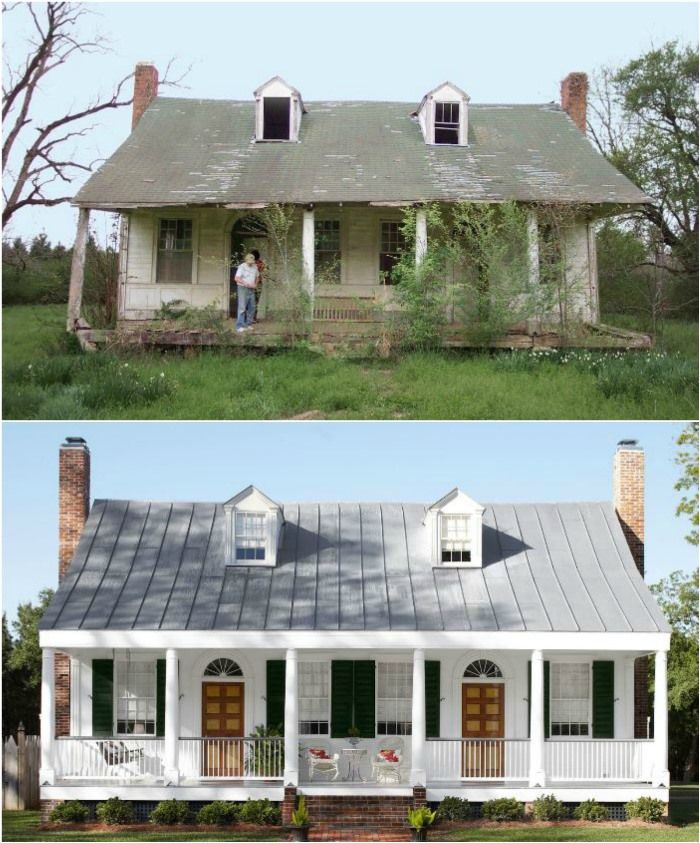

Home equity loans can be a great option for home improvement projects

A home equity loan can be a great option to finance your renovations. This loan will help you make improvements to your home and increase it's value. The loan will allow you to reap the benefits as long you pay the monthly payments.

Home equity loans are a great option for home improvements, but you need to consider all the pros and cons before applying. You should remember that you can lose your home if your loan is not paid on time. Improve your credit rating if you want to avoid foreclosure. By making timely payments, paying off debt and disputing any negative information on your credit report, you can avoid foreclosure. You can make your house more valuable and sell it faster by renovating.

Home equity loans offer a great way to get rid of credit card debt

Home equity loans can help you eliminate your credit card debt. They have lower interest rates that most credit cards. You can use them to consolidate multiple credit cards balances and make it easier to track your payments. Home equity loans have their drawbacks.

People with good credit are usually eligible for home equity loans. If you have bad credit, you will likely have to pay a higher interest rate on a home equity loan. This is because the interest on a home equity loan is tax deductible if you use the money to make improvements to your home. A tax professional should be consulted to help you determine if a home-equity loan is right.

FAQ

Are flood insurance necessary?

Flood Insurance covers flooding-related damages. Flood insurance helps protect your belongings and your mortgage payments. Learn more about flood insurance here.

What are the drawbacks of a fixed rate mortgage?

Fixed-rate loans have higher initial fees than adjustable-rate ones. You may also lose a lot if your house is sold before the term ends.

What time does it take to get my home sold?

It depends on many factors, such as the state of your home, how many similar homes are being sold, how much demand there is for your particular area, local housing market conditions and more. It can take anywhere from 7 to 90 days, depending on the factors.

Can I get a second mortgage?

Yes. However, it's best to speak with a professional before you decide whether to apply for one. A second mortgage is used to consolidate or fund home improvements.

What amount of money can I get for my house?

This varies greatly based on several factors, such as the condition of your home and the amount of time it has been on the market. The average selling price for a home in the US is $203,000, according to Zillow.com. This

Statistics

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How to find an apartment?

When moving to a new area, the first step is finding an apartment. This process requires research and planning. This involves researching and planning for the best neighborhood. You have many options. Some are more difficult than others. Before renting an apartment, you should consider the following steps.

-

Data can be collected offline or online for research into neighborhoods. Online resources include Yelp. Zillow. Trulia. Realtor.com. Local newspapers, real estate agents and landlords are all offline sources.

-

Find out what other people think about the area. Yelp. TripAdvisor. Amazon.com have detailed reviews about houses and apartments. You can also find local newspapers and visit your local library.

-

For more information, make phone calls and speak with people who have lived in the area. Ask them what they liked and didn't like about the place. Ask for their recommendations for places to live.

-

Check out the rent prices for the areas that interest you. Renting somewhere less expensive is a good option if you expect to spend most of your money eating out. You might also consider moving to a more luxurious location if entertainment is your main focus.

-

Find out more information about the apartment building you want to live in. How big is the apartment complex? How much does it cost? Is it pet friendly? What amenities does it have? Can you park near it or do you need to have parking? Are there any rules for tenants?