If you're planning to purchase a house during a house recession, there are a few things you should know. These factors include declining home prices, rising inventories, and first-time buyers. Lenders will need to make sure that borrowers can afford their loans. A lack of affordability could lead to a loss of many buyers that will have ripple effects on the economy.

Inflation-fighting mode

The Fed is currently in an inflation-fighting mode. This means that interest rates could rise unless the Fed can maintain a stable inflation rate. The Fed is acknowledging the cost of inflation and weighing on consumer confidence. The Fed is not looking to limit the economy, although inflation may slow down by itself.

Inflation reduction involves a number of steps. The first is tightening financial regulations, which will lead to a decrease in house prices. Loan rates have risen sharply, stock prices have dropped, and the dollar has strengthened in foreign exchange markets. These steps could take up to a year.

Falling home prices

The 2008-2009 Great Recession had a significant impact on real estate markets. As the economy suffered, so did the housing market, which saw the average home value drop by 5% every year. In comparison, the recessions of the 1980s and 2001 had similar effects, but housing prices increased more modestly.

As home prices decline, less people will be in a position to purchase homes. Some areas may experience a faster decline than others. Holiday areas with new construction could be especially hard hit. In addition, smaller cities will also be affected. For example, Austin, TX or Phoenix, CA, as well as Seattle, WA and Sacramento, CA may be more affected than the rest of the country.

Effect of Fed rate increases

Recent Fed rate increases have slowed the housing market. The nation's most awaited market has been affected by its actions in more ways. First, consumers feel less pressure to purchase when interest rates are rising rapidly. This causes a drop in economic growth and an increase in unemployment. Additionally, inflation and unemployment are in an inverse relationship. Inflation leads to higher prices. This is known as stagflation.

Higher mortgage rates are responsible for the impact Fed rate hikes have on the housing market. The average 30-year fixed-rate mortgage rate is currently at 6.25%. This represents a nearly 50% increase over the previous year's 3.5%. Rising interest rates make home purchases more expensive for many, particularly first-time buyers and people with low incomes.

FAQ

Can I purchase a house with no down payment?

Yes! Yes. There are programs that will allow those with small cash reserves to purchase a home. These programs include FHA, VA loans or USDA loans as well conventional mortgages. You can find more information on our website.

What are the drawbacks of a fixed rate mortgage?

Fixed-rate mortgages have lower initial costs than adjustable rates. Also, if you decide to sell your home before the end of the term, you may face a steep loss due to the difference between the sale price and the outstanding balance.

Can I get a second loan?

Yes, but it's advisable to consult a professional when deciding whether or not to obtain one. A second mortgage is used to consolidate or fund home improvements.

What is the maximum number of times I can refinance my mortgage?

This will depend on whether you are refinancing through another lender or a mortgage broker. You can typically refinance once every five year in either case.

How much does it take to replace windows?

Replacement windows can cost anywhere from $1,500 to $3,000. The total cost of replacing all your windows is dependent on the type, size, and brand of windows that you choose.

What is the average time it takes to get a mortgage approval?

It all depends on your credit score, income level, and type of loan. It generally takes about 30 days to get your mortgage approved.

Statistics

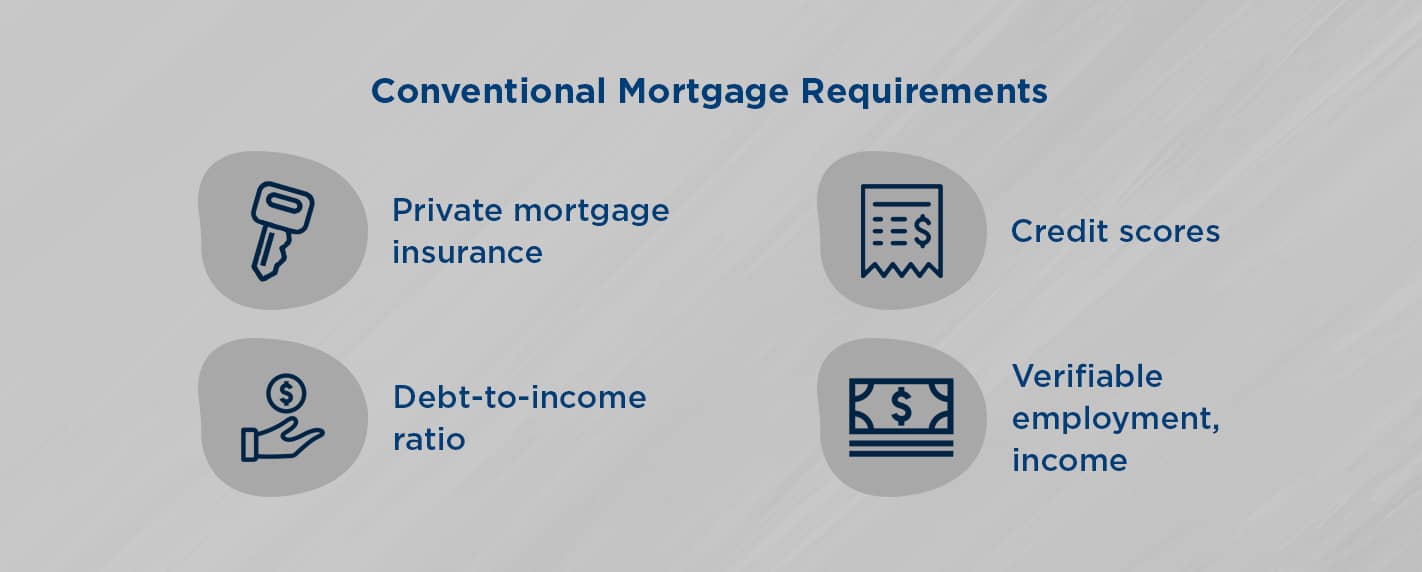

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

External Links

How To

How to become a broker of real estate

An introductory course is the first step towards becoming a professional real estate agent. This will teach you everything you need to know about the industry.

Next, pass a qualifying test that will assess your knowledge of the subject. This involves studying for at least 2 hours per day over a period of 3 months.

You are now ready to take your final exam. You must score at least 80% in order to qualify as a real estate agent.

All these exams must be passed before you can become a licensed real estate agent.