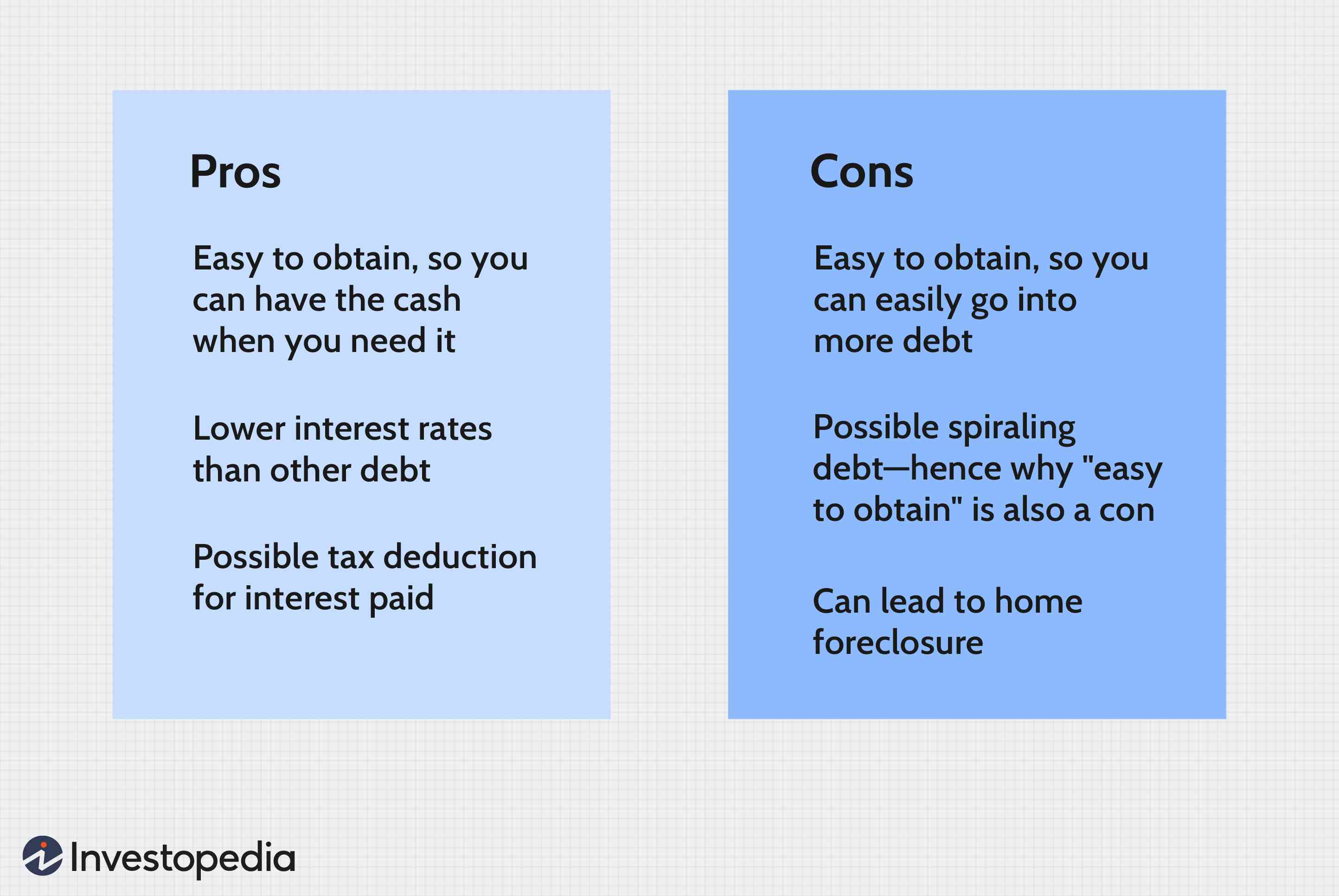

When comparing conventional vs VA loan, there are several factors to consider. These include down-payment requirements, mortgage insurance, as well funding fees. If you are a veteran, you can use these loans to save on your housing expenses and eliminate the need to pay PMI. In addition, these loans do not require down payments, which can reduce your total housing costs.

Convenient loan vs. VA loan

The down payment can be a big difference between a VA loan or a conventional mortgage. Conventional mortgages require that borrowers pay at least 3 per cent of the purchase price. By contrast, a VA loan requires no down payment. This is a great advantage for those who don’t want to make large down payments. According to Bankrate data, 36 percent of Americans do NOT own their homes. This is due in large part to the lack of money for a downpayment.

Another major difference between conventional loans and VA loans is the funding fee. A VA loan does not require private mortgage insurance, which protects the lender in the event of default. VA loans also allow borrowers flexible payback terms that include a graduated repayment structure.

Requirements to make a down payment

The principal difference between VA loans or conventional loans lies in the down-payment requirement. Conventional loans require 20% down payment. They are best suited to purchase investment property or vacation homes. VA loans can only be approved for primary residences. Furthermore, conventional loans are more flexible and can be used to purchase a second home or an investment property.

For VA loans, the down payment can be as little as 3%. Many military personnel choose to contribute a portion of the down payments, particularly if they are able to afford it. The down payment will help reduce the loan's funding fee, while it will eliminate PMI.

Insurance for mortgages

Mortgage insurance is necessary if you're planning on buying a house. Most conventional loans require private mortgage insurance, also called PMI. If you default, you will have to pay this insurance to the lender. This insurance can cost as much as 2% of the loan amount each year. VA loans do not require mortgage insurance. VA loans are not required to have mortgage insurance because they are funded by a trust that is government-backed.

VA mortgage loans have many advantages. These loans have low interest rates, no down payment and flexible eligibility criteria. VA mortgage loans can also be used to finance non-traditional lines of business, such as rent history, utility bills and other accounts. You may also be able to get approved with a credit score that is higher than 620.

Fees for funding

There are many distinctions between funding fees for a VA loan and a conventional loan. Conventional loans usually require private mortgage insurance (PMI), while VA loans do not. Both types require funding fees. This fee can be paid at closing, or rolled into the loan. It costs between 0.5% and 3.6% of the loan amount.

Funding fees for a VA loan are mandatory under federal law. These fees help protect the VA home loan program in the event that a borrower defaults on the mortgage. The fee amount varies depending on the type of loan and veteran's status. However, certain veterans are exempt from the fee. However, funding fees for conventional loans are not required by law. The private mortgage insurance for conventional homebuyers and other fees must be paid.

FAQ

How many times can I refinance my mortgage?

This is dependent on whether the mortgage broker or another lender you use to refinance. In either case, you can usually refinance once every five years.

How long does it take to sell my home?

It all depends upon many factors. These include the condition of the home, whether there are any similar homes on the market, the general demand for homes in the area, and the conditions of the local housing markets. It takes anywhere from 7 days to 90 days or longer, depending on these factors.

How can I tell if my house has value?

If you have an asking price that's too low, it could be because your home isn't priced correctly. Your asking price should be well below the market value to ensure that there is enough interest in your property. You can use our free Home Value Report to learn more about the current market conditions.

Is it possible for a house to be sold quickly?

You may be able to sell your house quickly if you intend to move out of the current residence in the next few weeks. But there are some important things you need to know before selling your house. First, find a buyer for your house and then negotiate a contract. The second step is to prepare your house for selling. Third, advertise your property. You should also be open to accepting offers.

How much money do I need to purchase my home?

It depends on many factors such as the condition of the home and how long it has been on the marketplace. Zillow.com shows that the average home sells for $203,000 in the US. This

Statistics

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

External Links

How To

How to Locate Houses for Rent

Moving to a new area is not easy. But finding the right house can take some time. When it comes to choosing a property, there are many factors you should consider. These include location, size, number of rooms, amenities, price range, etc.

You should start looking at properties early to make sure that you get the best price. Consider asking family, friends, landlords, agents and property managers for their recommendations. This will give you a lot of options.