A Home equity credit line (HELOC), is a credit card that is tied to your equity in your home. It's a good choice for older homeowners. There are some downsides to this credit card. Here are the pros & cons of this card.

Home equity line credit

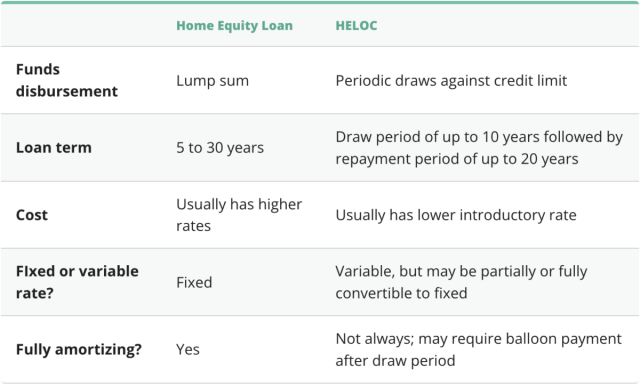

Home equity loans are secured by your equity in your home. You can borrow anywhere from 60% to 85% depending on which lender you choose. These loans are flexible and offer lower interest rates. However, they do have their drawbacks.

While a home equity line credit can be a good financial option, there are some pros and con's that you need to know. It is a loan and you will have to pay interest immediately. If you don't use the funds for a specified period of time, some lenders may charge an inactivity fee.

It's a credit line that is tied to your equity in your home.

HELOCs are revolving credit lines similar to credit cards that are tied to equity in your home. You can use it to pay off high-interest debts or for large purchases. You can borrow up to the amount that you have. This type of credit has an interest rate that is lower than most other types of loans. You might even be eligible for tax deduction.

Your HELOC can be used for major purchases and for vacations. It can also be used for reducing high-interest debt, paying for a new car, or even paying unexpected expenses. However, you must remember that the credit line is tied to your home's equity, and you should only use it for major purchases. Lenders will examine your ability and financial obligations, as well your ability as the credit limit.

This is a great option for seniors.

A HELOC is a revolving line of credit. This allows seniors to borrow money without having to make a down payment. These loans are secured with the homeowner's equity. Lenders can take over the home if you are unable to pay the loan payments on time. HELOCs can also help finance education expenses for your children and grandchildren. It can be used for home improvements, or to pay medical bills.

HELOCs also offer low interest rates. HELOCs are significantly cheaper than reverse mortgages, and they offer greater flexibility. However, there are some downsides.

It can be used in consolidating debt

A HELOC allows you to consolidate debt and simplify finances. The HELOC allows you to consolidate all of your debts and can reduce the interest rates on each account. A HELOC typically comes with lower interest rates than a credit card or a secured personal loan. Citizens offers two repayment options. They also support you at every stage of the process. You can use your equity to repay your high-interest debt.

You can use a HELOC to pay off high interest credit card balances. You can make your payments more flexible because it has a longer draw time than a credit cards. You can make additional payments towards the principal balance of your HELOC to reduce your interest payments. Another advantage of using a HELOC to consolidate debt is that it improves your credit score.

It can also be used to purchase a new home.

HELOCs can only be used to purchase a second house. You pay no interest for the amount you use. The flexibility of HELOCs makes them very attractive. You can use the equity in your home to pay down your debt, and the income from the investment property can help offset the debt. If you have sufficient income to cover the mortgage payments, you may be eligible to buy the second home with the income that you get from it. You must be aware however that the housing market is constantly changing.

You may need additional capital to cover the down payment or other expenses if you are looking to purchase a second house. HELOCs can be used to offset equity that you have already built in your current home. A HELOC cannot be taken out against the equity in your current home.

FAQ

Do I need to rent or buy a condo?

Renting could be a good choice if you intend to rent your condo for a shorter period. Renting will allow you to avoid the monthly maintenance fees and other charges. On the other hand, buying a condo gives you ownership rights to the unit. You have the freedom to use the space however you like.

How do I know if my house is worth selling?

If your asking price is too low, it may be because you aren't pricing your home correctly. If you have an asking price well below market value, then there may not be enough interest in your home. Our free Home Value Report will provide you with information about current market conditions.

Do I require flood insurance?

Flood Insurance covers flooding-related damages. Flood insurance can protect your belongings as well as your mortgage payments. Find out more information on flood insurance.

Do I need a mortgage broker?

A mortgage broker may be able to help you get a lower rate. Brokers are able to work with multiple lenders and help you negotiate the best rate. However, some brokers take a commission from the lenders. Before you sign up, be sure to review all fees associated.

How long will it take to sell my house

It all depends upon many factors. These include the condition of the home, whether there are any similar homes on the market, the general demand for homes in the area, and the conditions of the local housing markets. It takes anywhere from 7 days to 90 days or longer, depending on these factors.

What amount should I save to buy a house?

It all depends on how long your plan to stay there. You should start saving now if you plan to stay at least five years. You don't have too much to worry about if you plan on moving in the next two years.

How can I calculate my interest rate

Market conditions impact the rates of interest. The average interest rate over the past week was 4.39%. The interest rate is calculated by multiplying the amount of time you are financing with the interest rate. If you finance $200,000 for 20 years at 5% annually, your interest rate would be 0.05 x 20 1.1%. This equals ten basis point.

Statistics

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How to Find Houses to Rent

People who are looking to move to new areas will find it difficult to find houses to rent. Finding the perfect house can take time. When it comes to choosing a property, there are many factors you should consider. These factors include location, size and number of rooms as well as amenities and price range.

You should start looking at properties early to make sure that you get the best price. Consider asking family, friends, landlords, agents and property managers for their recommendations. This will allow you to have many choices.