You should understand how a home equity line-of-credit works if you are considering borrowing it. This type of revolving line of credit is secured by your home and comes with a set repayment period and interest rate. You must be a homeowner and have equity in your home to get approved. This means that the total amount you owe on your home must be less than the market value of your house. In addition, your lender will look at your debt-to-income ratio and credit score to determine whether or not you are a good candidate for this type of loan.

Revolving form of credit secured by your home

A home equity credit or HELOC (home equity line of credit) is a revolving credit facility from a lender which allows you to borrow against the equity of your home. This type of credit can be used for large-scale debt consolidation or to pay off high-interest bills. The interest paid on these loans is also tax-deductible.

A home equity line credit is only available to homeowners who have equity in their homes. The market value of your home must equal the amount you owe. Lenders will also consider your debt-to-income ratio, credit score, and history of paying your bills on time.

A home equity credit line can be used to help pay for major expenses, such as home repairs, medical bills, and education. Although the credit line can help you meet your monthly expenses it is not a good idea to be aware of the potential risks. You should have an emergency fund in place for when you borrow more than you can pay back.

Repayment period

The amount of the loan and equity in the home will determine the repayment period of a home equity credit line. The maximum loan amount is the same for all borrowers. However, the repayment period will vary depending on the amount of the loan and the equity in the home. Calculating the monthly repayment period of a HELOC will help you figure it out quickly.

A home equity line credit repayment period has two phases. The draw period is usually between 10 and 15 years. During this period, you'll make payments on the interest and principal of the line of credit. The repayment period follows the draw period.

Lenders can vary the repayment terms for home equity lines of credit. For example, a HELOC may allow you to make interest-only payments during the draw period, and a home equity payment plan may allow you to make principal-and-interest payments after the draw period. This will reduce your monthly payments.

Interest rate

There are many factors that can affect the interest rate of a home equity credit line. The margin is based on various factors, including the loan to value ratio, credit qualification, and property state. The interest rate is usually lower when the loan is opened but may rise as the loan is used more frequently.

The maximum amount you are allowed to borrow on a home equity credit line depends on the value of your home, the amount you owe on the mortgage and your income. This simple calculation can help you estimate how much money you can borrow. For example, if you owe 50% of the value of your home, you could borrow up to $20,000.

While a 5-year home equity line credit interest rate may be competitive with other rates in the market, it is better than others. You will still have to pay a monthly fee. The rate depends on your credit score, but the lowest rates are generally available for well-qualified borrowers with a loan-to-value ratio of 80% or higher. Credit scores of 740 and higher are required in order to qualify.

FAQ

What's the time frame to get a loan approved?

It depends on several factors such as credit score, income level, type of loan, etc. Generally speaking, it takes around 30 days to get a mortgage approved.

What are the benefits associated with a fixed mortgage rate?

With a fixed-rate mortgage, you lock in the interest rate for the life of the loan. This ensures that you don't have to worry if interest rates rise. Fixed-rate loans have lower monthly payments, because they are locked in for a specific term.

How many times may I refinance my home mortgage?

This is dependent on whether the mortgage broker or another lender you use to refinance. In both cases, you can usually refinance every five years.

Is it possible for a house to be sold quickly?

It might be possible to sell your house quickly, if your goal is to move out within the next few month. There are some things to remember before you do this. First, you will need to find a buyer. Second, you will need to negotiate a deal. The second step is to prepare your house for selling. Third, it is important to market your property. You should also be open to accepting offers.

How do I calculate my interest rate?

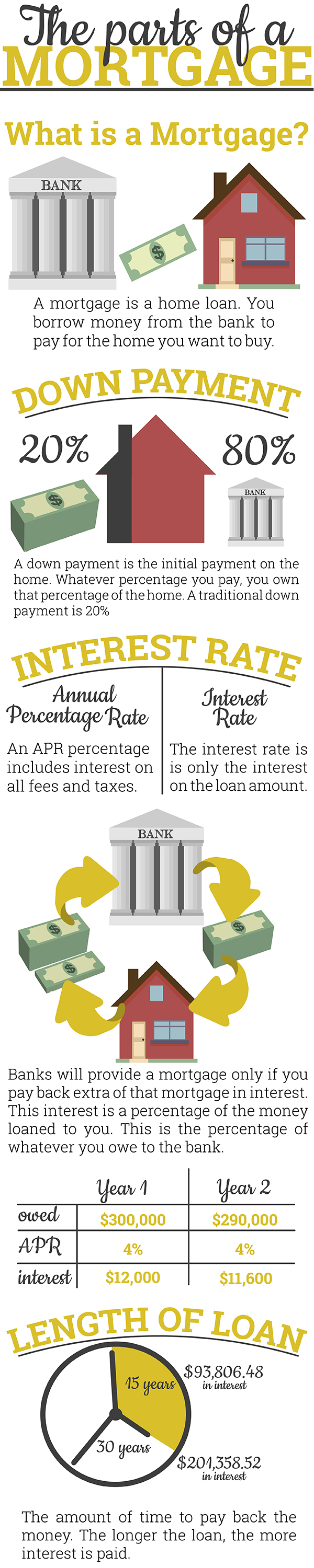

Market conditions influence the market and interest rates can change daily. The average interest rate during the last week was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. For example, if you finance $200,000 over 20 years at 5% per year, your interest rate is 0.05 x 20 1%, which equals ten basis points.

Should I rent or purchase a condo?

Renting could be a good choice if you intend to rent your condo for a shorter period. Renting saves you money on maintenance fees and other monthly costs. On the other hand, buying a condo gives you ownership rights to the unit. The space is yours to use as you please.

Is it possible to get a second mortgage?

However, it is advisable to seek professional advice before deciding whether to get one. A second mortgage is often used to consolidate existing loans or to finance home improvement projects.

Statistics

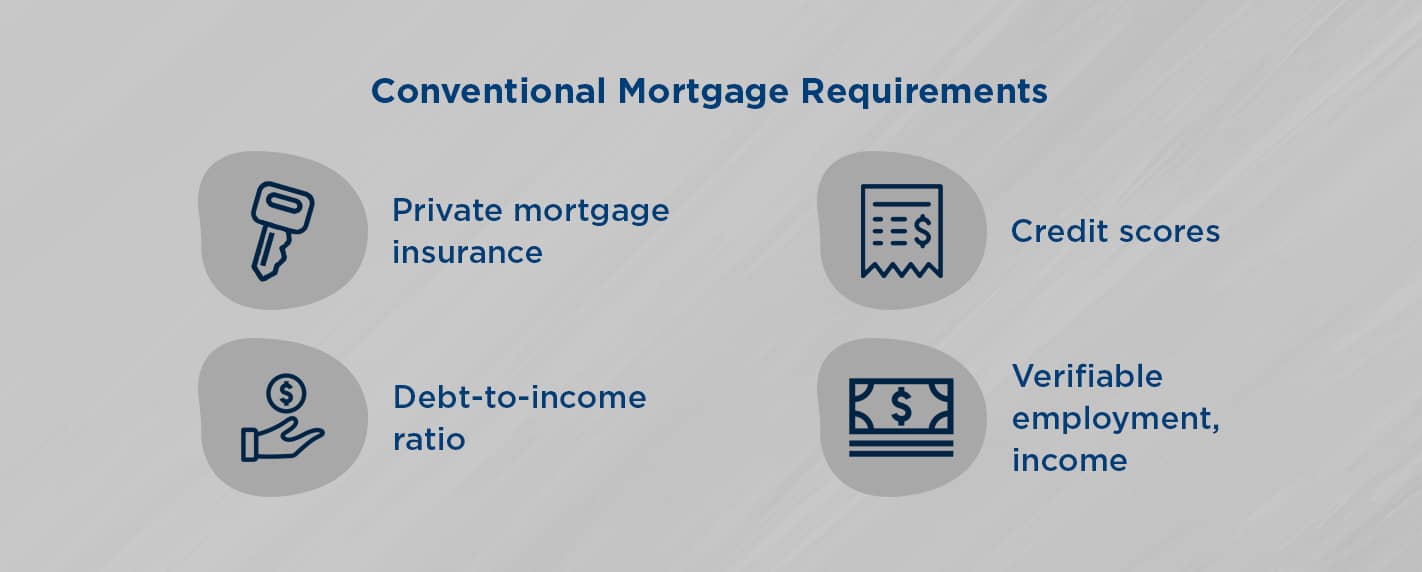

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

External Links

How To

How to become an agent in real estate

An introductory course is the first step towards becoming a professional real estate agent. This will teach you everything you need to know about the industry.

The next thing you need to do is pass a qualifying exam that tests your knowledge of the subject matter. This requires you to study for at least two hours per day for a period of three months.

After passing the exam, you can take the final one. To be a licensed real estate agent, you must achieve a minimum score of 80%.

All these exams must be passed before you can become a licensed real estate agent.